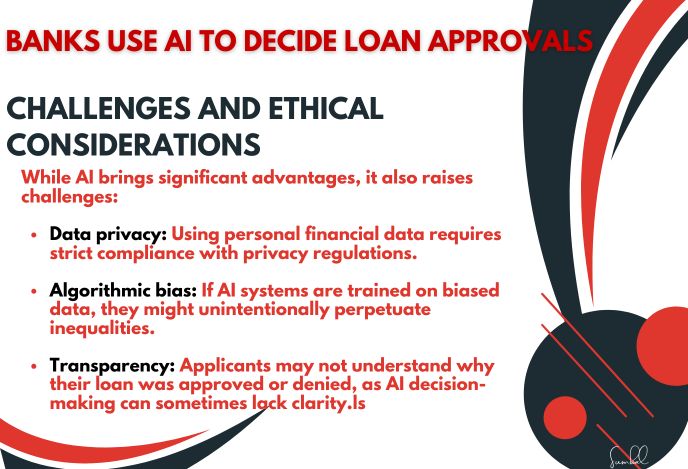

Conventional loan approvals could be faster, but they involve a lot of paperwork and require manual evaluations. Today, they are done with the help of AI, which helps banks and other financial institutions make much faster, more accurate, and, most importantly, informed decisions on loan applications. With the ability to process massive datasets, the algorithms enable the accurate evaluation of creditworthiness and loan repayment risks. This article explains how AI is transforming the loan approval process.

1. Examining financial information and credit scores

One of AI's new functions is to analyze borrowers' creditworthiness. In the old paradigms, credit scoring was widely used, but it did not give a complete picture of an applicant’s creditworthiness. AI systems delve deeper into data and provide a bigger picture by examining the following:

- Credit history: With the ability to look at previous borrowing history, repayment, and defaults.

- Spending habits: Monthly expenditure, savings, and expenditure on items of daily necessity and luxuries.

- Income stability: Examining income stability and job tenure using banking or payroll information records.

2. Faster Loan Processing

Another striking area is AI's capability to work on applications rapidly. AI can review loan application documents and make approval determinations within a few minutes.

For instance, instead of spending days, weeks, or even months waiting for their applications to be manually approved, applicants could be approved instantly based on AI results. This would not only improve the overall customer experience but also enable the banks to address many applications at once.

3. Impacting Accuracy and Bias

This comes as AI systems that have replaced loan officers are technically inclined to reduce bias and human mistakes. Conventional loan officers may end up making biased decisions. On the other hand, AI assesses talents based on statistics and agreed-upon standards, eliminating biases in the process.

Machine learning systems make decisions based on previous choices and outcomes and then modify these decision-making models to enhance accuracy. This has implications for the bank, including a reduced number of false rejections and better risk assessment.

4. Expanding Access to Loans

Through AI, banks can now lend to people who may not necessarily qualify for credit scores as per the conventional rating. For example:

- Alternative data analysis: AI considers various external sources of information, such as a person's ability to pay rent, utility bills, and even online purchases, to determine creditworthiness.

- Microloans: Self-learning algorithms enable banks to profitably make small loans at virtually no cost, thus supporting low-income consumers.

It enables banks to give credit to clients once locked out, improving the flow of credit in the economy.

5. Assessment of Fraud and Risk

AI evaluates not only the creditworthiness of an applicant but also the likelihood of fraud within a given application. By comparing application information with usual patterns and contrasting income details, AI solutions help recognize possibly fraudulent applications.

Furthermore, it analyzes the chances of default by studying past repayment behaviors. It assists banks in determining correct interest rates and other loan conditions to minimize possible risks and make loans more affordable for end-users.